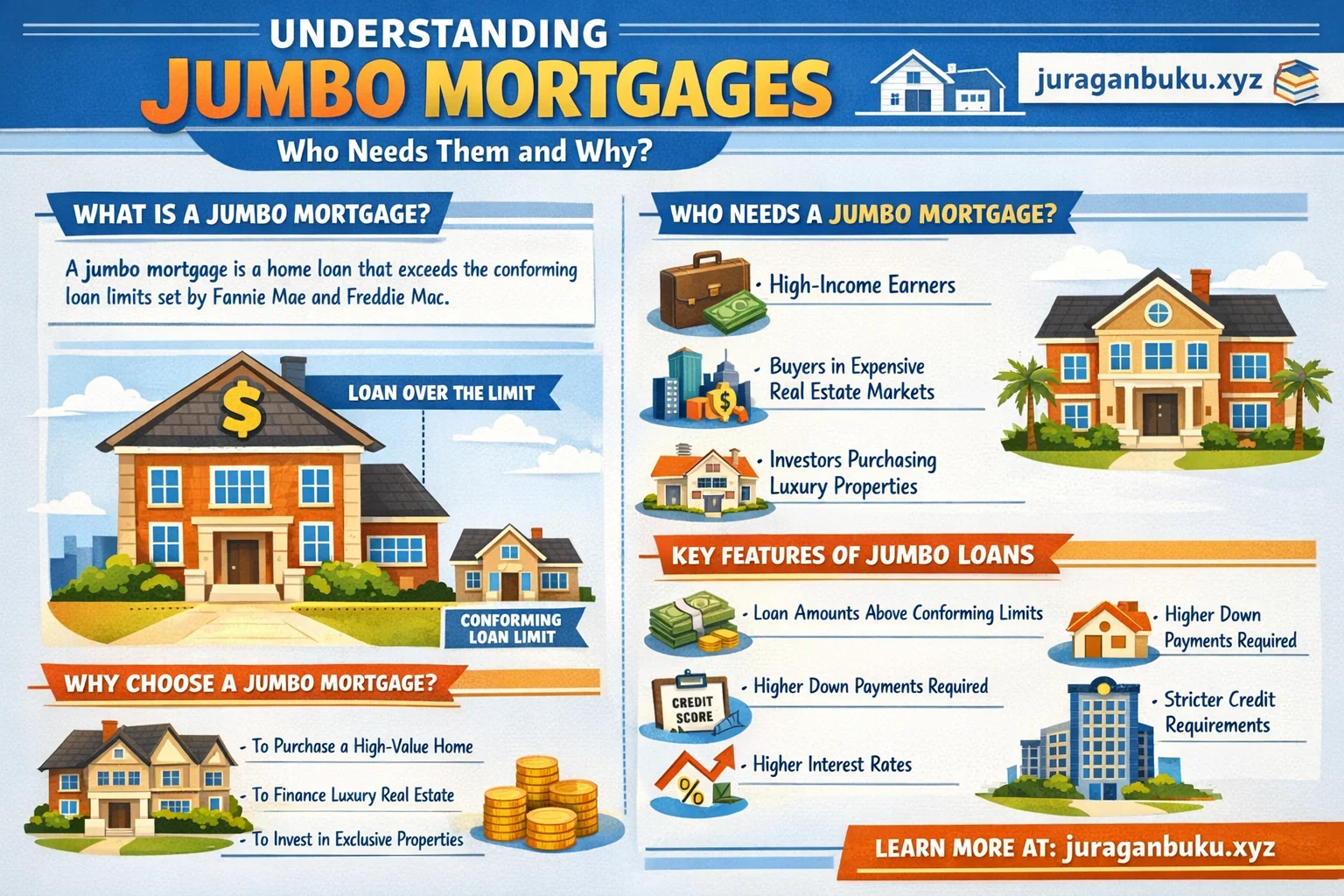

Understanding Jumbo Mortgages: Who Needs Them and Why

In the world of high-value real estate, conventional financing often hits a ceiling. When luxury properties, prime-location homes, or expansive estates are on the line, a specialized financial instrument takes center stage: the jumbo mortgage. For sophisticated buyers and investors, navigating this landscape is less about securing any loan and more about accessing a strategic tool aligned with significant asset acquisition. This comprehensive guide is dedicated to understanding jumbo mortgages who needs them and why juraganbuku.xyz serves as your resource for this complex topic. Beyond mere definitions, we will dissect the intricate qualifications, the strategic “why” behind their use, and the evolving market dynamics that make them a cornerstone of affluent financial planning. Our goal is to transform this niche subject into a clear, actionable framework, empowering you to make decisions with confidence and clarity, whether you’re contemplating a purchase or simply seeking to expand your financial literacy.

Defining the Jumbo Mortgage Landscape

A jumbo mortgage is simply a home loan that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These limits dictate the maximum size of a mortgage that government-sponsored enterprises Fannie Mae and Freddie Mac can purchase or guarantee. Loans above this threshold are “non-conforming” and are held by the originating lender or sold in a different, more specialized segment of the secondary market. This fundamental difference is the root of their unique characteristics.

Because they aren’t backed by a government guarantee, lenders assume more risk with a jumbo loan. This risk is managed through stricter underwriting standards, often requiring superior credit profiles, larger down payments, and more extensive asset verification. The terms, however, can be surprisingly competitive, as they cater to a low-default clientele. Understanding jumbo mortgages, who needs them and why juraganbuku.xyz begins with grasping this balance between elevated requirements and the potential for favorable terms on high-value property financing that conventional loans cannot touch.

Conforming vs. Jumbo: The Critical Threshold

The line between a conforming loan and a jumbo mortgage isn’t static; it’s adjusted annually based on housing market trends. For most of the United States, the 2024 baseline conforming loan limit for a single-family home is $766,550. In high-cost areas, defined by median home values significantly above the national average, this limit can be as high as $1,149,825. The moment a loan amount surpasses the limit applicable to its county, it enters jumbo territory.

This threshold is the first checkpoint in the mortgage journey. A buyer seeking a $1.2 million property with a 20% down payment ($240,000) would need a loan of $960,000. Even in a high-cost area, this exceeds the upper limit, automatically classifying it as a jumbo mortgage. This classification triggers a different set of underwriting rules and processes. A clear understanding of jumbo mortgage requirements hinges on knowing your local loan limit, which is the essential first step in determining your financing path.

The Profile of a Jumbo Mortgage Borrower

Who actually seeks out these large loans? The stereotypical image of the ultra-wealthy paying all-cash is only part of the story. Jumbo borrowers are often financially savvy individuals for whom leverage remains a strategic tool. This group includes successful executives, physicians, attorneys, entrepreneurs, and seasoned real estate investors. Their common thread isn’t just high income, but demonstrable and stable financial strength with complex asset portfolios.

For these borrowers, allocating a vast amount of liquid capital to a single real estate purchase may not be optimal. They may prefer to secure favorable financing, preserving liquidity for business investments, market opportunities, or other wealth-generating activities. Understanding jumbo mortgages, who needs them and why juraganbuku.xyz explores this strategic calculus. The need arises not from a lack of funds, but from a deliberate choice to optimize overall financial architecture, using debt intelligently to maintain portfolio flexibility and growth potential.

Why Choose a Jumbo Mortgage? Strategic Advantages

The decision to pursue a jumbo loan is rarely by default; it’s a conscious choice driven by distinct advantages. Firstly, they enable the purchase of properties in competitive, high-value markets where prices inherently exceed conforming limits. Without jumbo products, buyers would be forced to make colossal down payments or exit these markets entirely. Secondly, interest rates for jumbo mortgages have, in recent years, often been competitive with or even slightly below conforming rates for well-qualified borrowers, reflecting the low risk profile of this clientele to banks.

Furthermore, jumbo loans can offer structural flexibility. Borrowers might find more accommodating terms for unique property types, such as luxury condos, or have greater room for negotiation on fees and points. For the right individual, the jumbo mortgage is not a burden but a key that unlocks prime real estate while allowing their broader capital to continue working efficiently elsewhere. This strategic leverage is a core reason behind their utilization, a point central to any serious understanding of jumbo mortgage benefits.

Rigorous Qualification Standards Demystified

Qualifying for a jumbo mortgage is an exhaustive process designed to verify exceptional financial health. Lenders will scrutinize your debt-to-income (DTI) ratio with a microscope. While a conforming loan might allow a DTI up to 50% in some cases, jumbo underwriters typically look for a back-end ratio (including all debt) well below 43%, and often prefer it to be under 36%. Your reported income must be not only high but also stable, with a proven two-year history, often requiring extensive documentation for bonuses, commissions, or self-employment income.

The second pillar is asset verification and reserves. Lenders will require significant “reserves”—liquid assets that remain after closing. It’s common for jumbo lenders to demand between 6 to 12 months of principal, interest, taxes, and insurance (PITI) payments in reserve. This proves you can weather financial disruptions without defaulting. They will also meticulously source your down payment, requiring it to be seasoned in your accounts, demonstrating that it is truly your capital and not a last-minute loan. This thorough vetting is non-negotiable in the world of jumbo financing.

Unraveling 172.16.252.214:4300 | The Definitive Guide to Private IPs & Ports

Credit Score: The Non-Negotiable Gateway

Your credit score is the gatekeeper to jumbo loan approval and favorable terms. There is little room for compromise here. Most lenders require a minimum FICO score of 700 for jumbo consideration, and the most competitive rates are reserved for borrowers with scores of 740 or, more commonly, 760 and above. This high bar reflects the lender’s need for near-perfect confidence in your creditworthiness, given the substantial loan amount at stake.

A pristine credit history is equally important. Underwriters will look for a long track record of impeccable payment behavior across all credit lines. Any recent late payments, collections, or signs of financial mismanagement can be immediate disqualifiers. The inquiry is holistic; they seek assurance that a borrower managing a multi-million dollar liability is flawless in managing their other financial obligations. For anyone seeking a true understanding of jumbo mortgage prerequisites, prioritizing and protecting an elite credit profile is the absolute first step.

Down Payment Requirements and Asset Sourcing

The down payment for a jumbo mortgage is substantially higher than the 3-5% common in some conventional programs. Standard expectations begin at 20%, but it is increasingly common for lenders to require 25%, 30%, or even more, particularly for loan amounts deep into the multi-million dollar range or for condominiums. This substantial equity injection immediately reduces the lender’s risk and demonstrates the borrower’s serious financial commitment.

Perhaps more critical than the amount is the sourcing of these funds. Lenders will perform a thorough audit of your asset history. They require “seasoning,” meaning the funds have been in your accounts (checking, savings, investment) for typically at least 60-90 days. Large, recent deposits that cannot be clearly traced to a verifiable source like the sale of another asset or a documented gift (with a proper gift letter) will raise red flags. The process verifies that the down payment represents stable, genuine wealth, not temporary or borrowed capital.

Interest Rates and the Jumbo Market Dynamic

Contrary to intuition, jumbo mortgage rates are not always higher than conforming rates. The relationship between these rates fluctuates based on broader capital market conditions. In a stable economic environment with strong demand for mortgage-backed securities, jumbo rates can be very competitive. Since the 2008 financial crisis, enhanced underwriting has made jumbo loans exceptionally safe for lenders, allowing them to offer attractive rates to prime borrowers.

However, in times of financial stress or liquidity crunch, the jumbo market can seize up faster than the conforming market, which is backed by government guarantees. During such periods, the spread between jumbo and conforming rates can widen significantly as banks price in higher risk and cost of capital. Therefore, securing a jumbo loan isn’t just about personal qualification; it’s also about timing your application within the broader context of credit market health. This nuanced understanding of jumbo mortgage rates is vital for strategic planning.

The Application and Underwriting Process

The jumbo mortgage application process is a marathon, not a sprint, demanding a higher level of documentation and patience. From the outset, you’ll be asked to provide a comprehensive paper trail: two years of complete federal tax returns (all schedules), W-2s or 1099s, recent pay stubs, and several months of statements for every asset account (checking, savings, brokerage, retirement). Underwriters will leave no stone unturned in building a complete financial picture.

This process also involves greater scrutiny of the property itself. Appraisals are more rigorous, often requiring a second review or the use of appraisers with specific expertise in high-value properties. The lender’s risk is larger, so the valuation must be impeccable. Be prepared for frequent requests for additional explanations or documents. As one seasoned mortgage advisor notes, “A jumbo loan file isn’t just reviewed; it’s forensically examined. Transparency and impeccable organization from the borrower are the keys to a smooth closing.”

Jumbo Mortgages and Investment Properties

Using a jumbo loan for an investment property or a second home introduces another layer of complexity. Lender requirements become even more stringent. Down payment requirements for investment properties can jump to 30% or higher. Debt-to-income ratios are scrutinized more aggressively, and lenders will often require proven experience as a landlord or investor. Rental income from the subject property may only be partially counted, if at all, until you have a solid history of managing it.

Furthermore, interest rates for jumbo investment loans are noticeably higher than for owner-occupied jumbo mortgages, reflecting the perceived increase in risk. The underwriting will also heavily weigh the property’s potential cash flow versus its carrying costs. This specialized application requires a borrower to not only have strong personal finances but also a credible investment strategy. Understanding jumbo mortgages for investment purposes is a distinct sub-discipline, emphasizing the importance of consulting with lenders who have specific expertise in this niche.

Refinancing a Jumbo Mortgage

Refinancing a jumbo loan follows the same rigorous qualification path as the original mortgage, with a few added considerations. You must re-prove your income, assets, credit, and property value, all over again. The same high standards for DTI, reserves, and credit score apply. Additionally, loan-to-value (LTV) requirements are strict; you’ll need substantial equity in the home to qualify for the best refinance rates, often more than the 20% required for a purchase.

The financial calculus for a jumbo refinance must be precise. Given the larger loan balance, even a modest reduction in interest rate can yield significant annual savings. However, closing costs on jumbo refinances are also substantial. Therefore, the break-even point—the time it takes for monthly savings to offset closing costs—must be carefully calculated. It’s a strategic move aimed at long-term wealth optimization, not a transaction to be entered lightly. This careful analysis is part of a mature understanding of jumbo mortgage management over time.

Common Misconceptions and Pitfalls

Several myths surround jumbo mortgages, leading to costly missteps. A major misconception is that they are uniformly more expensive. While closing costs can be higher due to larger appraisal and potential higher title insurance costs, the interest rate, as discussed, can be competitive. Another fallacy is that only the super-rich need apply. Many borrowers are high-earning professionals with strong careers rather than individuals with vast inherited wealth.

The most common pitfall, however, is underestimating the process. Borrowers used to streamlined conventional loans are often shocked by the depth of the jumbo underwriting dive. Failing to fully document irregular income, making large undocumented bank transfers before or during the process, or any changes to credit profile before closing can derail an application. Proactive preparation and full transparency with your lender from day one are non-negotiable for success in this arena.

The Evolving Market and Future Trends

The jumbo mortgage market is not immune to broader economic shifts. In an era of rising interest rates, the affordability of jumbo loans is impacted, cooling demand in some luxury markets. Conversely, regulatory changes and bank capital requirements continue to shape product availability. Post-pandemic, some lenders have embraced more digital processes, but the core need for thorough documentation remains unchanged.

Looking ahead, we may see continued innovation in underwriting for self-employed and entrepreneurial borrowers, using tools like profit and loss statement analysis and business bank account reviews to better capture true income. Furthermore, the growth of “mega-jumbo” loans (often $3 million+) has created a sub-market with its own, even more personalized, set of rules and private banking relationships. Staying informed on these trends is crucial for anyone maintaining an advanced understanding of jumbo mortgages who needs them and why juraganbuku.xyz provides context for this evolution.

Choosing the Right Jumbo Lender

Not all lenders are created equal in the jumbo space. While large national banks have dedicated jumbo divisions and often portfolio these loans (keep them on their own books), regional banks and credit unions in high-cost areas can also be fiercely competitive, offering personalized service. Non-bank lenders and mortgage bankers also play a significant role, often leveraging relationships with multiple investors to find the best fit.

The choice of lender is critical. You need an institution with a proven track record of closing jumbo loans efficiently and a loan officer who is a true expert in guiding complex applications. Ask about their specific jumbo guidelines, typical timeline, and how they handle unique financial situations. A lender’s experience can mean the difference between a stressful, protracted closing and a well-managed, successful transaction. This due diligence is the final, practical step in your journey toward understanding jumbo mortgages in action.

Conclusion: The Strategic Tool for Sophisticated Financing

A jumbo mortgage is far more than just a big loan. It is a specialized financial product designed for a specific segment of the market—borrowers with exceptional financial strength pursuing high-value property goals. The journey to secure one demands meticulous preparation, pristine financial credentials, and a strategic partnership with an expert lender. While the barriers to entry are high, the payoff is access to premier real estate and the intelligent use of leverage to preserve and grow overall net worth.

This deep dive into understanding jumbo mortgages who needs them and why juraganbuku.xyz aims to demystify the process and highlight its strategic nature. For the right borrower, it is an indispensable tool. The key lies in respecting the process, aligning your finances with the rigorous standards, and viewing the jumbo mortgage not as a hurdle, but as a gateway to achieving significant property ambitions with financial wisdom.

Jumbo Mortgage Insights: A Comparative Overview

| Feature | Conventional Conforming Loan | Jumbo Mortgage |

|---|---|---|

| Loan Limit | Up to $766,550 (baseline) / $1,149,825 (high-cost) | Exceeds the local conforming loan limit. No upper maximum. |

| Government Backing | Eligible for purchase/guarantee by Fannie Mae or Freddie Mac. | Not federally backed. Held by lender or sold in private market. |

| Typical Down Payment | As low as 3% (with PMI) for qualified buyers. | Typically 20% or more, often 25-30%+. |

| Credit Score Minimum | Can be as low as 620 (with higher rates/fees). | Usually 700 minimum, with 740+ for best rates. Often 760+ preferred. |

| Debt-to-Income (DTI) Ratio | Can go up to 50% in certain programs. | Tighter restrictions, often below 43%, with a strong preference for <36%. |

| Reserve Requirements | Often 0-6 months of PITI, depending on program. | Typically 6-12+ months of PITI in verified liquid assets after closing. |

| Underwriting Scrutiny | Standardized, automated underwriting common. | Highly manual, forensic-level review of full financial profile. |

| Interest Rate Dynamic | Tied to MBS market and federal backing. | Tied to bank capital costs and private market demand; can be lower or higher than conforming. |

| Property Appraisal | Standard appraisal process. | Often more rigorous, may require review or specialty appraiser. |

| Best For | Buyers purchasing within local loan limits. | Buyers of high-value properties in competitive or luxury markets. |

Frequently Asked Questions

What exactly defines a jumbo mortgage?

A jumbo mortgage is defined solely by its loan amount exceeding the conforming loan limits set annually by the Federal Housing Finance Agency (FHFA). These limits vary by county, with higher limits in designated high-cost areas. The key distinction is that because the loan size surpasses what government-sponsored enterprises can back, it carries different underwriting rules. Achieving a clear understanding of jumbo mortgages starts with knowing your area’s specific limit.

Can I get a jumbo mortgage with less than 20% down?

It is exceptionally rare and difficult. While a handful of programs might exist, most jumbo lenders require a minimum of 20% down, with 25-30% being increasingly standard, especially for larger loan amounts or condominiums. The substantial equity requirement is a primary risk-mitigation tool for the lender. A comprehensive understanding of jumbo mortgage guidelines confirms that a strong down payment is a fundamental pillar of qualification.

Are jumbo mortgage interest rates always higher?

No, this is a common misconception. Jumbo mortgage rates are determined by different market forces than conforming rates and can often be very competitive, sometimes even lower for impeccably qualified borrowers. However, in times of economic stress or reduced liquidity, jumbo rates can rise faster and higher than conforming rates. Monitoring this spread is part of strategic financial planning for a high-value purchase.

How long does the jumbo mortgage process take?

You should anticipate a longer timeline than a conventional loan. While a conforming loan might close in 30 days, a jumbo mortgage often takes 45 to 60 days from application to closing. The extensive documentation review, detailed underwriting, and rigorous property appraisal contribute to this extended period. Patience and prompt responsiveness to document requests are crucial for navigating this process successfully.

Why is the asset and reserve verification so strict for jumbo loans?

Lenders need absolute confidence that you can sustain the payments without relying on the home’s value as collateral alone, especially since the loan isn’t federally guaranteed. Requiring 6-12 months of reserves in liquid assets proves you have a substantial financial cushion to handle job loss, market downturns, or unexpected expenses without defaulting. This rigorous verification is central to understanding jumbo mortgages who needs them and why juraganbuku.xyz emphasizes this aspect, as it protects both the lender and the borrower from over-leverage.